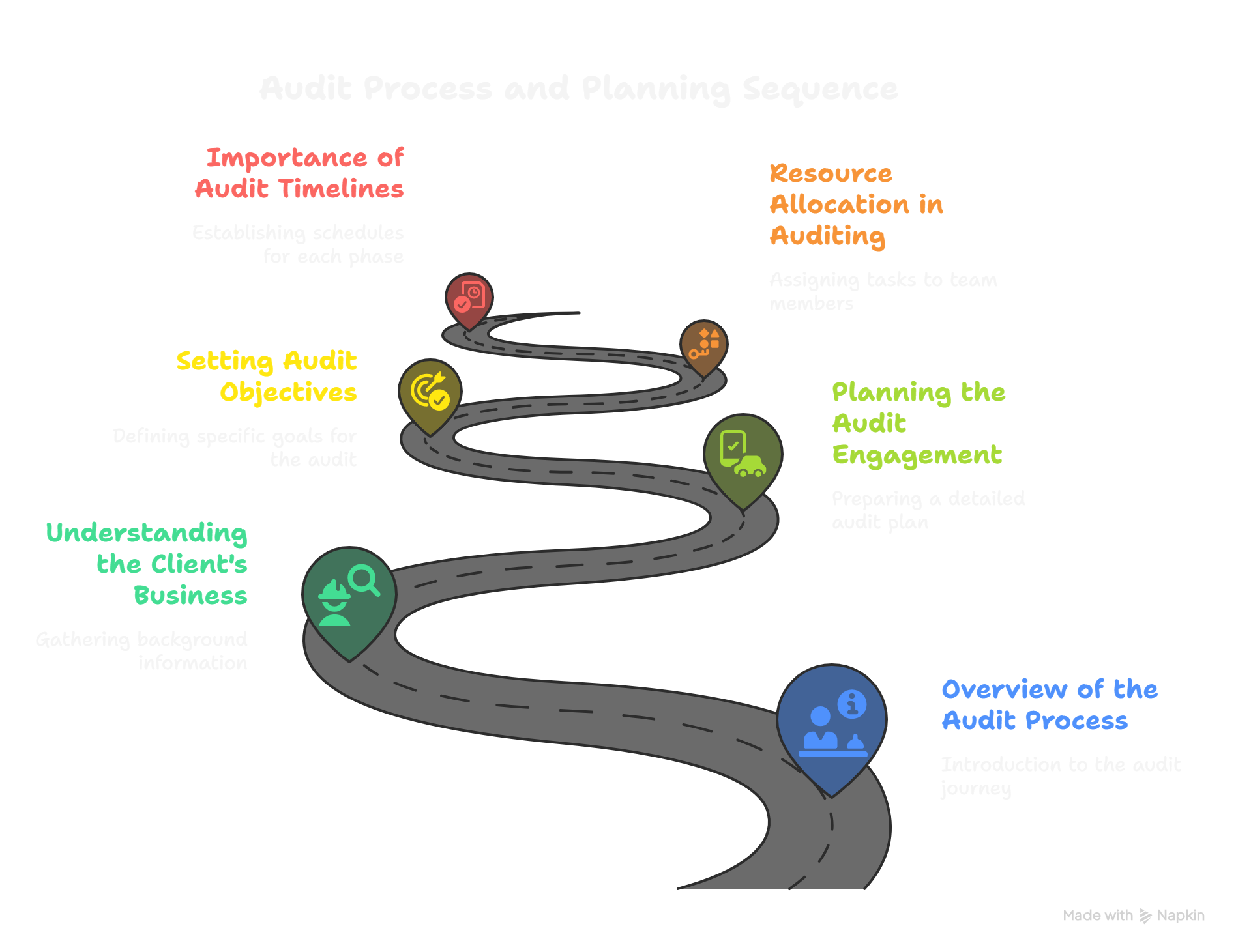

Application of Audit in Real World

3.3 Application of Standards in Real Audits

Let’s step into Lukman’s shoes as he takes on a new audit assignment at a client’s head office. The aroma of kopi o fills the meeting room as Lukman and his audit team lay out their plans for the day. As usual, Lukman keeps a copy of the International Auditing Standards (ISAs) at hand—his reference for any sticky situations.

Applying ISAs During Planning

Before diving into the audit itself, Lukman gathers his team. “Alright guys, according to ISA 300, we need a detailed audit plan. That means we’ll document our understanding of the business, set our objectives, and allocate resources based on risk.” The team discusses the client’s expansion into online sales, which introduces new risks around revenue and inventory. By following the standard, they create an audit plan tailored to these specific risks, ensuring nothing important is overlooked.

Evidence Gathering, Powered by the Standards

As the audit work kicks off, Lukman remembers a key point from ISA 500: always obtain sufficient and appropriate audit evidence. So, when testing sales transactions, Lukman doesn’t just take the client’s word for it. He reviews invoices, matches them with delivery orders, and even requests customer confirmations for unusual transactions. The audit standard gives him the authority to be thorough, not just trust but verify.

When Uncertainty Arises

Halfway through, Lukman stumbles upon a discrepancy in the bank reconciliation. The client’s finance officer insists it’s just a timing issue. Lukman, guided by ISA 240 (auditor’s responsibility relating to fraud), probes deeper. He asks for supporting documents, checks for patterns in previous years, and considers if management is exerting pressure to hide mistakes. The ISAs remind him: always exercise professional skepticism, especially when things don’t add up.

Reporting and Wrapping Up

With the fieldwork complete, Lukman and his team prepare the audit report. ISA 700 outlines exactly how this report should look—the layout, wording, and what must be included for clarity and transparency. This consistency not only reassures the client but also ensures that anyone reading the report, whether in Malaysia or overseas, can trust its findings.

A Real Example

Lukman recalls a time when his adherence to the standards prevented a major oversight. During an audit of a retail business, he noticed a sudden spike in cash sales. Instead of glossing over it, he relied on ISA 315 (identifying and assessing risks of material misstatement) and performed extra procedures. It turned out some sales had been recorded twice, inflating revenue. Without following the specific standard, Lukman might have missed this error.

In summary, Lukman’s story shows that applying auditing standards isn’t about ticking boxes. It’s about having a solid framework that directs you to ask the right questions, seek the right evidence, and deliver objective, high-quality work—every single time.